Reassessing India’s Regulatory Framework For Cross-Border Corporate Structuring And Tax Avoidance

Introduction

Today, India stands at the crossroads of law and economics. As Indian businesses and high-net-worth individuals increasingly invest through jurisdictions such as Mauritius, Singapore, and the United Arab Emirates, the ongoing pattern of what is called ‘global expansion’ often conceals a more subtle intent: to bypass local laws under the guise of cross-border legitimacy. Additionally, these corporate structures are not just tools for tax benefits or offshore capital access; they are intentionally designed legal mechanisms that operate within the law but go against its spirit.

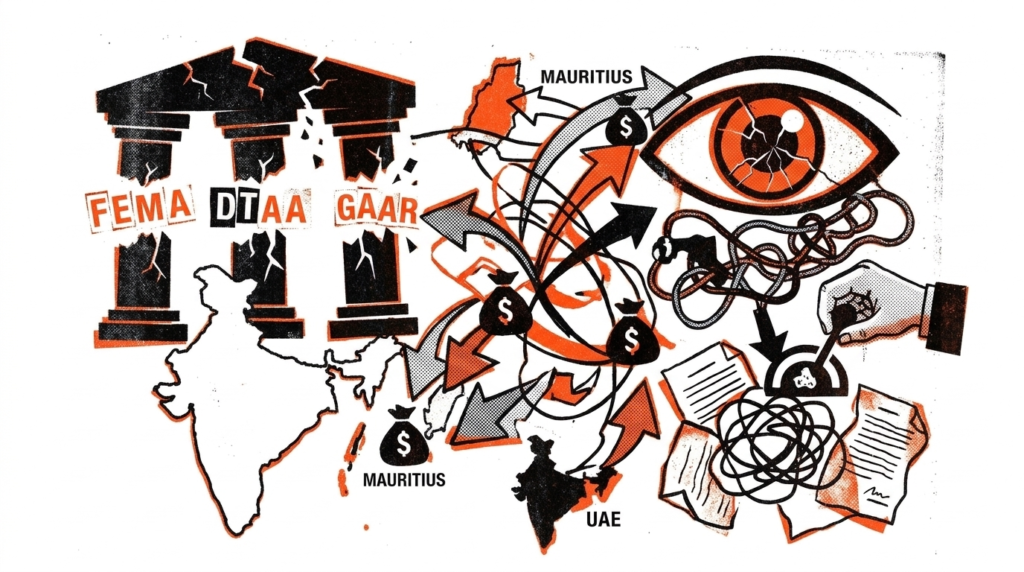

This is not a matter of a regulatory vacuum but of incoherent regulation, where fragmented oversight allows systematic evasion. The trio of Indian laws under the Foreign Exchange Management Act (FEMA), Double Taxation Avoidance Agreements (DTAA), and General Anti-Avoidance Rules (GAAR) offers broad statutory coverage. However, each of these laws essentially functions as a separate regime. The outcome is a fragmented system where loopholes are not just discovered, they are created. In these cases, the law is followed more in appearance than in reality, which can only be described as “legally permissible illegality.”

It is not illegal to have offshore holding companies, shell companies, or trust structures that involve multiple layers of trustees. Rather, they are frequently deployed to obscure beneficial ownership, circumvent exchange controls, or facilitate round-tripping under the guise of foreign investment. The key issue is whether Indian law can deal with these structures that are technically compliant but strategically evasive.

Judicial precedent has merely added a layer of complexity. The Supreme Court’s decision in Azadi Bachao Andolan regarded Tax Residency Certificates (TRCs) as conclusive for treaty access, thereby applying a formalist approach to cross-border tax avoidance. GAAR, intended to counteract this approach, remains ambiguous and has been inconsistently enforced. Enforcement under FEMA exploits the limited authority delegated to authorised dealer banks, which are neither capable nor sufficiently empowered to function as a forensic financial regulator.

The cumulative effect is a system that punishes after the impact has occurred. The regulatory response in India is reactive, fragmented, and under-integrated. The global landscape is now characterised by financial engineering, and the lack of transparency means that enforcement based on trust and bureaucracy is not sustainable. A reorientation of regulatory philosophy is required, from passive rule enforcement to active economic investigation.

If this depletion of efficacy is allowed to continue, then the ramifications will be greater than lost tax revenue or the movement of capital: it will undermine the normative legitimacy of Indian law itself. Where compliance is performative, and enforcement is hesitant, the legal order starts to fray. India does not need more legislation—it needs better coordination, institutional cohesion, and regulatory intelligence that can view structure for substance, differentiate between innovation and moral hazard, and avoid hampering legitimate enterprise.

In a world where capital can access different faces and jurisdictions compete to erode regulatory boundaries, India needs to move away from regulatory defence towards affirmative assertion. The real issue is no longer whether these structures are legally acceptable; it is whether they are morally and institutionally acceptable in a system that professes to embrace equity, integrity, and sovereign control.

The Mechanics and Motivation Behind India’s Outbound Structuring

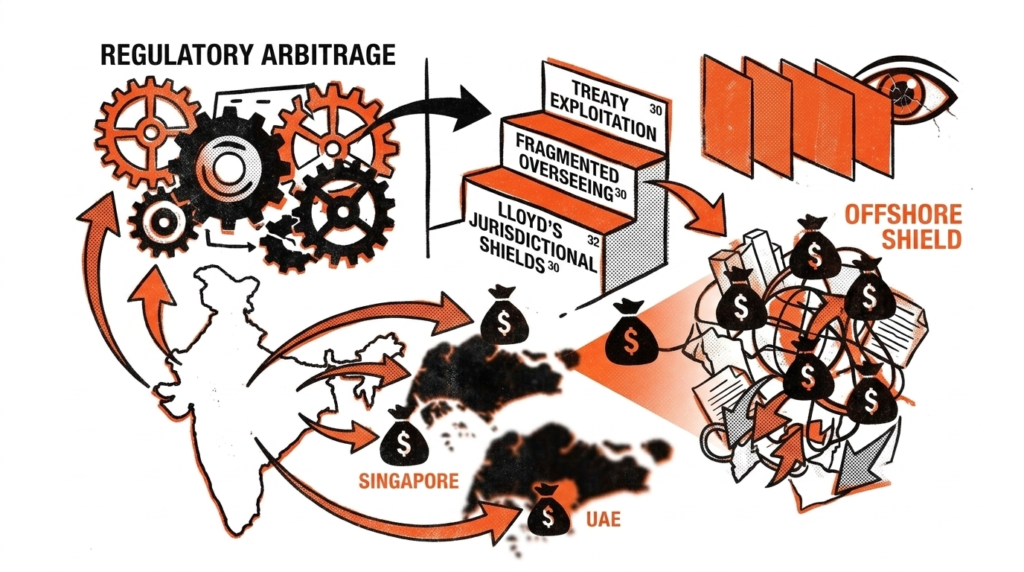

India’s outbound structuring is no longer merely a result of capital liberalisation; it has become a legally engineered strategy grounded in regulatory arbitrage, treaty exploitation, and fragmented jurisdictional oversight. Indian corporations and HNIs are increasingly riding cross-border structures for tax optimisation and to shield transactions from domestic regulatory visibility. The selection of jurisdictions like Mauritius, Singapore, and the UAE is a deliberate, calculated strategy to minimise scrutiny, to corrosively cloak beneficial ownership, and to technologically route funds through mechanisms that are legally inimical but economically artificial.

The preference for Mauritius finds its roots in the India–Mauritius Double Taxation Avoidance Agreement (DTAA), which, till its amendment by the 2016 Protocol, had provided that capital gains arising from the transfer of Indian securities shall be taxable only in Mauritius. The absence of capital gains tax there created a perfect zero-tax arrangement for entities investing in India by this route. Notwithstanding the use of source-based taxation under the protocol after April 1, 2017, the grandfathering of investments made before that date continues to give the jurisdiction relevance. The CBDT Circular No. 789/2000 further cemented the usability of this channel by stating that a valid TRC issued by Mauritius would constitute sufficient evidence of residence. This position was upheld by the SC in Union of India v. Azadi Bachao Andolan, where the Court favoured a formalist interpretation, stating that legitimate tax planning through treaty benefits cannot be invalidated on the grounds of motive.

Singapore presents a similar, albeit more structured, alternative. The India–Singapore DTAA, which had been amended in 2016 to follow the Mauritius protocol, initially did provide for similar exemptions from capital gains but now provides for source-based taxation with effect from transition. Singapore, however, remains relevant for its strong financial ecosystem, higher worldwide recognition, and timely compliance services. It requires only a minimum physical presence. That can be satisfied through, say, the appointment of nominee directors or the rental of office space. An added attraction is regulatory certainty. Its alignment with OECD BEPS Action Plans, at least in form, has enabled it to maintain the perception of substance, even when operational control resides outside its borders.

In recent years, the United Arab Emirates has become an important hub of outbound Indian structuring. India UAE DTAA contains an extensive amount of exemptions and lower rates of withholding tax. Until recently, the UAE was tax-free, with no corporate tax, capital gains tax, or personal income tax, meaning that Indian entities can easily set up holding companies that enjoy complete tax neutrality. The fact that disclosure of beneficial ownership in the UAE was not robust, in particular before the promulgation of its Economic Substance Regulations in 2019, made it a jurisdiction of choice for passive asset holding and round-tripping structures. The recent corporate tax in 2023 has not turned it off because of its generous carve-outs for free zones on free zones and group restructures.

These jurisdictions are typically combined in multi-level structures, forming a multi-layered setup that would insulate legal ownership from beneficial ownership. The most usual structure is to include a Special Purpose Vehicle (SPV) in Mauritius or Singapore, owned by a family trust or a closed foundation in one of the secrecy jurisdictions, such as the Cayman Islands or the British Virgin Islands. This layering, which is formally compliant, attenuates transparency and makes regulation tracing useless. Although round-tripping is prohibited by FEMA Regulations, especially the Foreign Exchange Management (Transfer or Issue of Any Foreign Security) Regulations, 2004, those authorised dealer (AD) banks are left with the responsibility of enforcing the regulation, and they have no investigating powers; enforcement depends on the declaration of the investor.

It is also through the use of trust structures, i.e., discretionary or irrevocable family trusts, that the identity of the settlor is hidden. Such trusts are often regulated in offshore jurisdictions where disclosures are lax and with minimal regulatory oversight. In the event of the effective retention of the literal control by the Indian settlor, separation at law is achieved by legal documental sequestration. Sections 89 and 90 of the Companies Act, 2013 mandate disclosure of beneficial ownership, whereas a lack of cross-border enforcement treaties creates barriers in the extraterritorial application of these, since they are intended to be direct, rather than international in scope.

There is an additional insulation through nominee directors. With the laws in Singapore and the UAE, many Indian promoters put residents of Singapore or the UAE as directors to fulfil formal requisites, but still have de facto control. Such setups show dubious intentions through the prism of beneficial ownership, but otherwise, the transactions are scarcely explored, unless money laundering or high-risk is involved. According to the Prevention of Money Laundering Act, 2002, and the Know Your Customer (KYC) norms issued by the RBI, ultimate beneficial ownership must be verified. However, regulators have no ready access to foreign corporate registries or trust deed documents that enjoy attorney-client privilege.

Round-tripping, namely the reinvestment of Indian-source capital into India through offshore vehicles that are considered foreign investors, may constitute the most important issue that should be considered by legal counsel. While technically prohibited under FEMA, such arrangements often escape detection due to the absence of real-time data sharing among RBI, SEBI, and tax authorities. In many instances, the inflow as FDI/foreign portfolio investment (FPI) is just re-branded Indian funds availing of the incentives secured by the foreign investment under the Indian law. The 2019 FEMA (Non-Debt Instruments) Rules tried to rationalise the investment routes, but it had created a gap in interpretations on beneficial ownership and control.

Legal Framework Governing Cross-Border Structuring in India

India’s regulatory framework for cross-border structuring is built on three pillars: the Foreign Exchange Management Act (FEMA), a network of Double Taxation Avoidance Agreements (DTAAs), and the General Anti-Avoidance Rule (GAAR). While designed to protect India’s tax base, these regimes operate in isolation, creating a system that is legally comprehensive but practically incoherent.

FEMA & the Outbound Direct Investment (ODI) Rules, 2022

Outbound Indian investment is regulated by the Foreign Exchange Management Act, 1999, and rules and regulations made thereunder, such as the Foreign Exchange Management (Overseas Investment) Rules and Regulations, 2022. The 2022 restructuring was knowledgeable and facile since it grouped investments into Overseas Direct Investment (ODI) and Overseas Portfolio Investment (OPI) and upgraded forms of compliance on monetary promises, ownership, and multiple-tiered organizations.

The new regime is now limiting the investments with greater than two levels of subsidiaries, due diligence on control and ownership of foreign entities, and prohibition of routing funds through jurisdictions listed as untrustworthy by the Financial Action Task Force (FATF). Although these technical improvements are on the way, structural constraints are hampering enforcement. The authorised dealer (AD) banks, the front-line enforcers, act more as facilitators rather than regulators. This does not give them the power to verify facts through forensics or carry out any independent investigation, but they are left to operate based on what has been disclosed by the investing entity.

Being an apex regulator, the Reserve Bank of India (RBI) does not have access to any real-time cross-border database or any common registry to access the Ultimate Beneficial Ownership (UBO) of different jurisdictions across borders. This merely makes the system reactive: the violations tend to manifest themselves when the money is through several foreign jurisdictions, each with its own asset-privacy and secrecy measures, so there is very little that is traceable.

While the 2022 framework introduces a filter against shell-layering, particularly in “non-cooperative” jurisdictions, the operative FATF list applied in India is limited in scope and rarely updated. In comparison, other jurisdictions, such as the UK or the EU, deploy machine-led transaction tracing systems that automatically red-flag abnormal routing or layered financial flows. The lack of predictive surveillance in India makes its structure friendly to anticipate complex offshore structuring.

Double Taxation Avoidance Agreements (DTAAs)

India’s treaty network comprises over 90 Double Taxation Avoidance Agreements, many of which include provisions for capital gains exemption, dividend repatriation, and tax-sparing credits. Initially, they were created on the assumption of no artifice placed to prevent double taxation, but it has frequently provided doubling of non-taxation, and in jurisdictions due to treaties, are used where there is nominal or no actual economic residence of members.

The India–Mauritius DTAA, before its 2016 protocol revision, allowed capital gains from Indian securities to be taxed only in Mauritius, where no such tax existed. This led to an influx of foreign consortium investment channelled through Mauritius, much of which was sustained by shell companies. What the Protocol of 2016 amended is the method of taxing the sources and introducing grandfathering in case the income occurred before April 1, 2017, and yet the source of the abuse is yet to be dealt with.

A similar pattern can be observed under the India-Singapore DTAA, where the exemption of capital gain was also permissible. Even though the treaty has been revised to fit into the Mauritius framework, its actual implementation is limited. The Limitation of Benefits (LoB) clause that was intended to sieve out shell structures demands that it must engage in authentic commercial operations in Singapore. Nevertheless, these claims are little under regulatory oversight. The substance is simulated by most entities through the use of minimal physical presence (e.g., rented office space or nominee directors), but in essence, it plays no real economic role.

In the example of India-UAE DTAA, the problem is more modern. Before the UAE corporate tax law was introduced in 2023, Indian companies had established holding companies in the UAE where they enjoyed almost complete tax exemption and low disclosure standards. Even under the new Economic Substance Regulations, which require minimum levels of activity, enforcement remains jurisdiction-specific and often a mystery. Nonetheless, the treaty still provides for undercharging withholding taxation within the international boundaries set out, as well as an exemption that can be taken advantage of until Indian regulators undertake more economic scrutiny of claims under the treaty.

India’s reliance on Tax Residency Certificates (TRCs) as the gateway for treaty access, although upheld in earlier judicial decisions, has become increasingly out of step with evolving international standards under the OECD’s Base Erosion and Profit Shifting (BEPS) Action Plan, especially the Principal Purpose Test (PPT). The treatment of a holistic inquiry into economic substance or beneficiary ownership in India is not yet full-scale enforcement of treaties, as formal compliance can be used in support of strategic evasion.

General Anti-Avoidance Rule (GAAR)

The General Anti-Avoidance Rule, under Chapter X-A of the Income Tax Act, 1961, was designed to target impermissible avoidance arrangements, defined as transactions where the primary purpose is tax avoidance and where the structure lacks commercial substance or involves misuse of tax provisions. GAAR empowers tax authorities to deny treaty benefits, disregard intermediaries, and recharacterize transactions in line with their economic reality.

GAAR has not gained much usage despite this extensive mandate. The regulatory squirm comes about due to its subjective triggers, lack of an exclusive appellate power, and the fear of retroactivity. It is only sparingly or infrequently enforced, and it is usually reserved when the case is high-profile or gross. Even in such cases, the ambiguity concerning procedural safeguards leaves the taxpayers and the tax officers with doubts.

More importantly, the GAAR is not structurally integrated. It does not have a working interaction with either FEMA or SEBI, or even with DTAA formats. A transaction that is tax-lawful under FEMA and the treaties can be caught by GAAR, and, thus, the resulting compliance regime can become contradictory to the point where neither regulator has exclusive jurisdiction or the primary power of interpretation.

As much as the Vodafone International Holdings case brought or brought forth the realization that India is prone to indirect transfer structuring and treaty shopping, the prospect of GAAR is still a dream in the making. Rather than serving as a systemic instrument to question the substance of transactions, it has continued to be exercised as a discretionary instrument used only selectively to a level that lacks a coherent administrative application that would discourage the structuring of transactions on tax grounds.

Loopholes, Latency, and Legal Blind Spots: The Structural Gaps

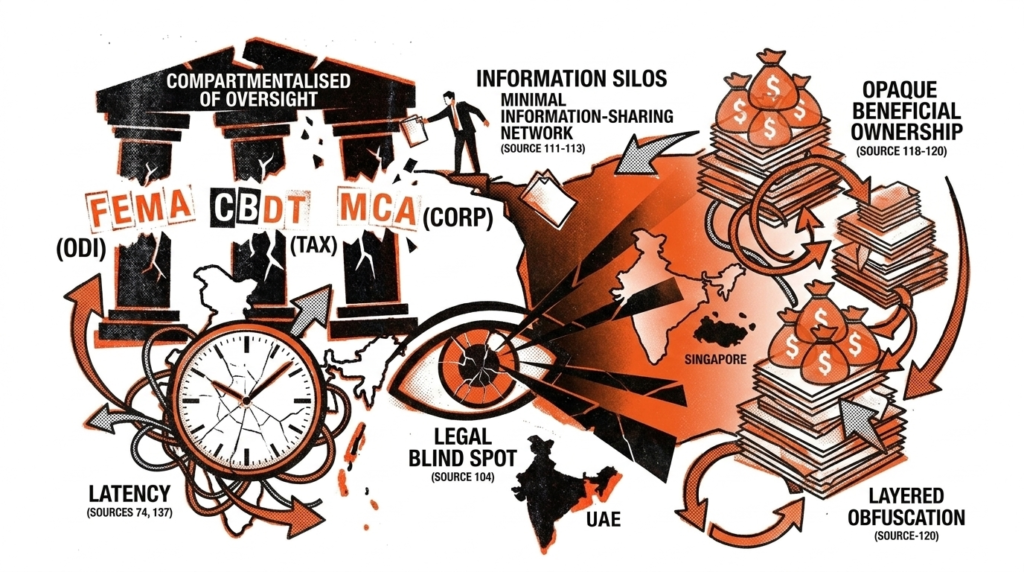

India’s legal architecture governing cross-border corporate structuring, though robust in appearance, is undercut by deep institutional fragmentation, reactive enforcement, and an overwhelming reliance on form-based compliance. The question is not whether the law is missing but whether the integrative regulatory capacity is lacking. Although laws such as the Foreign Exchange Management Act (FEMA), Income Tax Act (using the GAAR), and the corporate disclosures under the Companies Act operate as independent statutes, they hardly merge in a way that would serve to fully disincentivize offshore-based structuring done to circumvent taxes. This fragmentation facilitates the continuance of an environment of opacity, jurisdictional arbitrage, and passive regulation.

Jurisdictional Fragmentation and Regulatory Silos

One of the most foundational weaknesses in India’s regulatory infrastructure lies in the compartmentalisation of oversight. The Reserve Bank of India governs capital flows under the ODI regime; the Central Board of Direct Taxes (CBDT) interprets and enforces tax treaties and anti-avoidance norms; the Ministry of Corporate Affairs (MCA) handles beneficial ownership disclosures under the Companies Act; and the Securities and Exchange Board of India (SEBI) supervises foreign portfolio investment mechanisms like participatory notes. Nevertheless, these agencies use institutional silos and are involved in a minimal information-sharing network, and fail to integrate a cross-regulatory intelligence structure. This contributes to an atmosphere whereby, in case one authority sees abnormalities in the framework or possession, this knowledge is unlikely to prompt synchronized regulation in other authorities. A firm can receive a clean bill of health in ODI procedural filings in the same breath as a violation of the GAAR, only to be told that there is no single point of institutional contact to fill in the gap.

Opaque Beneficial Ownership and Layered Obfuscation

The challenge of tracing ultimate beneficial ownership (UBO) lies at the heart of illicit cross-border structuring. Indian promoters frequently establish multi-tiered structures involving intermediary entities in jurisdictions with high financial secrecy, such as the British Virgin Islands, Cayman Islands, or Mauritius. These structures are commonly designed to separate the legal form of control and the economic substance of control. Practically, this implies that the Indian UBO is buried many levels deep under the nominee directors, trust set-ups, or shell holding structures. Though India has disclosed beneficial ownership as mandatory under Section 90 of the Companies Act, such disclosure has no practical purpose when the chains have official addresses in offshore locations. ROC does not have visibility of foreign corporate registries or trust declarations, and there is no effective interoperability between foreign disclosures at the offshore and home structures. Consequently, national registrations provide an incomplete patchwork image that does not provide the whole picture of the beneficial ownership structure, leaving capital stuck to rotate offshore without having the slightest idea of the immediate repercussions.

Treaty Shopping through Minimal Compliance

A major enabler of structured tax avoidance is the strategic incorporation of entities in jurisdictions that offer favourable treaty terms, commonly referred to as treaty shopping. These jurisdictions are not selected for any operational rationale but merely to unlock lower withholding tax rates, exemption from capital gains, or other fiscal benefits under India’s network of Double Taxation Avoidance Agreements (DTAAs). Even after the treaties between India and Mauritius in 2016 and between India and Singapore were revised introducing the limitation-of-benefits clauses, such shopping still goes on in terms of ensuring that the threshold indicating the existence of a permanent establishment such as Tax Residency Certificates (TRCs), whether documents have Place of Effective Management (POEM) or even the formation of paper boards with the directors acting as nominees. Such formalistic tests are satisfied regularly with no substance of actual control or business activity within the treaty jurisdiction, and Indian authorities remain accepting them simply on their face. By such, they continue to enforce a jurisprudence which supports bare procedural satisfaction in comparison to material economic relationships, which defeats the anti-abuse purpose of the tax treaties.

The Legitimisation of Passive Capital Structures

The widespread use of Special Purpose Vehicles (SPVs) and offshore holding companies further accentuates the loopholes in India’s oversight regime. These entities often exhibit no revenue, assets, staff, or physical operations, yet enjoy full legal standing and treaty access. While such vehicles may be formally lawful, their economic substance is negligible. The continued dominance of form over substance in Indian enforcement practice—especially in accepting documentation like TRCs, board resolutions, or nominee agreements—legitimises these passive capital conduits. Moreover, enforcement agencies rarely challenge the functional validity of such structures unless a glaring red flag is raised through media or whistleblower disclosure. This regulatory reluctance to interrogate the underlying economic rationale of offshore holdings allows legally plausible yet economically hollow entities to facilitate round-tripping, base erosion, or tax arbitrage without meaningful challenge.

Comparative Jurisdictional Models: Striking the Balance Elsewhere

Across the globe, jurisdictions grappling with the abuse of cross-border corporate structuring have moved beyond mere formalistic compliance toward frameworks that foreground economic substance and systemic deterrence. In contrast, India’s regime still largely oscillates between reactive enforcement and piecemeal legislation. Conversely, the regime in India continues to remain either reactive enforcement or ad-hoc legislation in large parts. The trend seen worldwide is that of a greater conformity between the legal form and economic reality, resulting in paradigms that have not just taxed artificial structures but discouraged their creation by establishing them through design in a regulatory sense. A comparison of different legal frameworks, including the United Kingdom, the United States, Singapore, and multilateral laws, such as the Base Erosion and Profit Shifting (BEPS) of the OECD, has been beneficial in terms of understanding how the economic nexus, tax substance, and beneficial ownership are incorporated into legally binding requirements.

United Kingdom: Controlled Foreign Company (CFC) Regime

The United Kingdom’s approach rests heavily on the Controlled Foreign Company (CFC) regime, which imposes tax on passive income earned by offshore subsidiaries controlled by UK-resident entities, especially where such subsidiaries are located in low-or no-tax jurisdictions. The central thrust of the CFC regime is to disregard formal incorporation abroad if control and economic interest emanate from within the UK. Notably, the UK courts have taken a management and control test to identify tax residency, hence eliminating the possibility of tax deferral in passive offshore structures. Moreover, the UK has also conformed to the Significant People Function (SPF) test in its development of transfer pricing and risk allocation principles, so that the functions undertaken by key personnel in the UK are allocated to them in a way that does not depend on where the nominal incorporation has taken place. This substantive concept significantly differs from the procedural practice that is employed in India, where documentation like Tax Residency Certificates (TRCs) or Place of Effective Management (POEM) may easily be fabricated to exhibit the creation of artificial compliance.

United States: GILTI, Subpart F, and FATCA

The United States, in its bid to clamp down on tax base erosion, has implemented sweeping legislative instruments such as the Global Intangible Low-Taxed Income (GILTI) regime and the Subpart F provisions. These rules seek to tax passive income, intangible profits, and deferred earnings of foreign subsidiaries, even where such income is not repatriated. Subpart F, which has existed since the 1960s, already targets the passive income of Controlled Foreign Corporations (CFCs), while GILTI, introduced through the 2017 Tax Cuts and Jobs Act, goes further by taxing global profits that escape taxation due to strategic IP migration or income shifting. These provisions operate on the principle that income should not escape the tax net simply because it is routed through jurisdictions of convenience. Reinforcing these substantive standards are disclosure-centric statutes like the Foreign Account Tax Compliance Act (FATCA), which compels foreign financial institutions to report U.S. account holders and enforces cross-border information flows through reciprocal agreements. The United States’ ability to mobilize compliance from foreign jurisdictions through economic leverage remains unparalleled and provides a contrast to India’s limited enforcement infrastructure and dependence on self-disclosure.

Singapore: Economic Substance and Treaty Relief

Singapore’s model, while often characterised as “tax-friendly,” underscores the role of actual economic substance in extending tax benefits. For instance, merely incorporating a holding company in Singapore does not suffice for tax residency. The Inland Revenue Authority of Singapore (IRAS) requires demonstrable control and management within the country. These are among the requirements: the board must meet in Singapore; it must have operating personnel and office facilities locally and make decisions locally. The resistance to providing treaty relief or tax shelters to shells with no actual activities shows a policy stance that makes keeping it simple more important than looking good on paper. In a liberalised tax regime, Singapore imposes stringent terms to fund management and special purpose entities, a strategy that not only retains its international reputation, but also its local tax base.

Multilateral Frameworks: OECD BEPS, MLI, and Pillar Two

Multilateral efforts under the OECD’s BEPS framework, particularly the Multilateral Instrument (MLI), the Principal Purpose Test (PPT), and the recent Pillar Two agreement on a global minimum corporate tax, mark a significant shift in international tax jurisprudence. The MLI empowers jurisdictions to simultaneously amend bilateral treaties, thereby incorporating anti-abuse standards such as PPT, which denies treaty benefits where obtaining such benefits was the principal purpose of the arrangement. India has already joined the MLI system and has given notification on a number of its bilateral treaties to be revised. Nonetheless, it is still uncertain how the standards are to be enforced and litigation-ready in the domestic setting. Pillar Two, however, introduces the proposal of large multinational groups being subject to a minimum global corporate tax rate of 15 per cent, so as to eliminate the induced profit-shifting incentive by removing tax rate arbitrage. When such global standards are enforced strictly, they may be able to fill in enforcement gaps in the home country, such as India.

Lessons for India

These international models reveal a shared philosophy: tax integrity depends on aligning taxation with real economic activity. The key lesson for India is that while tools like GAAR and POEM exist, their effectiveness is crippled by a lack of institutional coordination and enforcement. Meaningful reform, therefore, depends less on new legislation and more on a fundamental upgrade of institutional capacity and data intelligence.

The Way Forward: Building a Smart, Substance-Oriented Structuring Framework

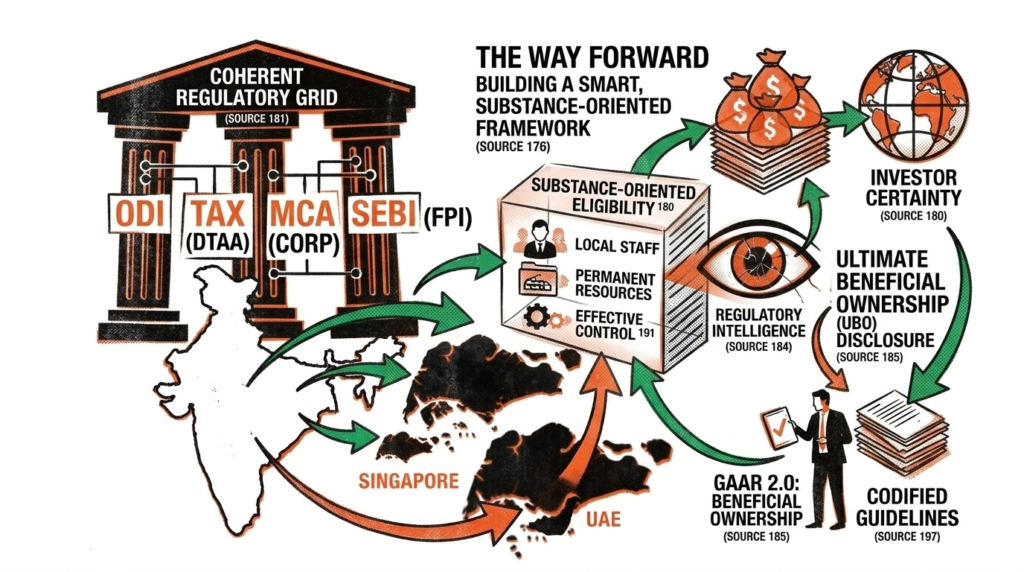

India’s regulatory response to cross-border corporate structuring has long suffered from a problem of posture; it focuses more on control than comprehension. Other nations whose exposure to capital flight and treaty abuse situations is comparable have turned to economic substance, whereas in India, the legal tactic is so procedural and responsive. The solution then is not to impose newer constraints on outbound investors, but to pursue a smarter, integrative-driven architecture that utilizes economic signaling, digital transparency, and legal certainty. India has lacked any legislative coverage but strategic convergence. To be able to take a modern structuring regime as a foundation thereof, three major pillars have to be used: cross-institutional coherence, substance-oriented eligibility, and investor certainty.

Unified Enforcement Through a Cross-Agency Regulatory Grid

One of the gravest structural failings of India’s regulatory framework is jurisdictional fragmentation. The Reserve Bank of India (for ODI), Central Board of Direct Taxes (for GAAR and treaty eligibility), Ministry of Corporate Affairs (for beneficial ownership disclosures), and SEBI (for participatory note oversight) operate as institutional silos. A forward-looking model requires an integrated enforcement grid. This is a centralized regulatory intelligence mechanism that will connect outbound capital dealings of firms, corporate shareholding patterns, and beneficial ownership databases in one platform, which is jointly utilized by different agencies. Such a framework should do more than gather information; it should correlate across fields, including ODI filings to income tax returns, shareholder data at the ROC versus foreign UBO filings, and provide warnings about risk areas based on destination jurisdiction and chain of control. The auditability and traceability can be increased alongside data integrity and regulatory oversight in real-time by embedding such records in a blockchain-connected interface.

Treaty Access Should Be Conditional on Demonstrable Economic Substance

While India’s engagement with the OECD’s Multilateral Instrument (MLI) and the Principal Purpose Test (PPT) signals an evolving stance toward anti-abuse standards, domestic enforcement of treaty access remains overly formalistic. Foreign holding structures continue to secure tax benefits merely by furnishing Tax Residency Certificates (TRCs) or minimal board presence. A more substantial change would be to incorporate treaty eligibility in the wider context of economic presence. An approach to implement this would involve the amendment of the Model Tax Convention and DTAAs to require concrete benchmarks, like the usage of local staff, possession of permanent resources, and effective control over the operation to allow access to the benefits offered in the treaty. Additionally, at the pre-assessment level, the PPT should be operationalized so that tax officers can make a substance-over-form assessment instead of litigating in a bid to attack post-abuse. This change would eliminate treaty shopping as an inherent design factor and would place India in line with best practices as experienced in other jurisdictions like Singapore and the UK.

GAAR 2.0: Clarity, Certainty, and Credibility

India’s General Anti-Avoidance Rule (GAAR), though ambitious in design, has been undercut by ambiguity, selective enforcement, and a lack of procedural integration. GAAR, should it ever be a credible deterrent, must be the subject of a second-generation reform-one that gives clarity of triggers, certainty of application, and credibility of enforcement. First, GAAR should be accompanied by codified interpretive guidelines that delineate the scope of “impermissible avoidance arrangements” in a manner consistent with global practices under the OECD BEPS framework. This will curb the broad discretion that is currently being given to assessing officers and fears of arbitrary application.

Second, procedural predictability would have to be entrenched by establishing a special appeals court or tribunal to deal with GAAR disputes. This kind of establishment would develop consistency in jurisprudence, speed up adjudication, and create confidence in investors.

Third, the credibility of the enforcement is determined by the fact that GAAR is joined with other pillars of regulation. Unless it is adjusted to the ODI framework in FEMA, the foreign portfolio control by SEBI, and the disclosure framework provided by the Companies Act, GAAR will be a solitary statute with minimal systemic impact. A “GAAR 2.0” must therefore not be used in isolation as a deterrent, but as part of a wider ecosystem in which tax avoidance will be considered alongside capital flows, ownership transparency, and corporate governance standards.

Overhauling ODI Norms to Disincentivize Capital Looping and Round-Tripping

The Overseas Direct Investment (ODI) guidelines under FEMA remain heavily focused on procedural compliance, board approvals, sectoral limits, or financial caps, but fail to capture the economic rationale of outbound investments. The next stage of reform must emphasize destination risk profiling and post-investment scrutiny. High-risk jurisdictions (especially those with nil corporate tax rates or opaque UBO regimes) must be subjected to pre-clearance requirements, compelling investors to disclose the intended purpose, projected activity timeline, and economic rationale of the proposed investment.

Incentivising High-Substance Outbound Structures: A Strategic Push, Not Regulatory Panic

While current reforms focus on curbing abuse, equal policy emphasis must be placed on enabling legitimate, value-accretive outbound investments. India must offer a fast-track approval route for outbound investments in strategic sectors such as renewable energy, deep-tech, semiconductors, and defence-linked R&D, especially when backed by Indian intellectual property or manufacturing capacity. These entities can be relieved of procedural barriers under ODI and extended treaty benefits under Bilateral Investment Treaties (BITs) as long as they conform to pre-determined norms of economic presence overseas. On the contrary, passive fund-transfer-driven ODI, usually channelled through the Cayman Islands, BVI, or Mauritius, with no commercial substance in between, should be left to a stricter test, rejection of capital, or withheld clearance. This will have a dual-channel: one to transit fast lanes on strategic capitals and scrutiny lanes respectively on suspect capitals. This is a shaded way of retaining the competitiveness of the Indian capital in the global spectrum on behalf of discouraging regulatory arbitrage.

Conclusion: Structuring, Sovereignty, and the Law’s Role

While cross-border corporate structuring is a legitimate global strategy, India’s fragmented legal ecosystem, split across the Income Tax Act, FEMA, and DTAAs, often conflates it with evasion. This lack of coherence has failed to discourage abuse and has instead created a climate of regulatory uncertainty and selective enforcement.

This article has shown that India’s current regime lacks both precision and alignment. It fails to differentiate between genuine outbound investment and artificial arrangements designed to round-trip or obscure beneficial ownership. Further, enforcement systems have been unable to keep pace with new structuring strategies; excessively formalistic tests (including the POEM or control-based standards) have been found incompatible with contemporary corporate mobility and the digital flows of capital. By contrast, other jurisdictions such as the UK and the US have built economic substance as a principle of governance directly into their tax laws, with a particular focus on matters of active control, operational footprint, and ensuring global tax alignment, through measures including GILTI, Subpart F, and the CFC provisions.

The path forward for India lies not in multiplying regulatory checks, but in designing a smarter, substance-driven framework that rewards transparency and penalises abuse without throttling global competitiveness. It is essential to have a coordinated structure where the rules of ODI, the thresholds of GAAR input, the eligibility of the treaty, and the aspect of corporate disclosures share the language of the regulation. Ambiguity needs to be dispelled with clarity: safe harbours, pre-determined thresholds, and appeal procedures can create certainty in the eyes of taxpayers and at the same time protect revenue.

Ultimately, India’s regulatory ambition must move from defensive gatekeeping to proactive goal-setting. The legal framework should empower legitimate structuring that aligns with national interest, be it through outbound investment in strategic sectors, or the use of Indian IP abroad, while surgically disincentivising hollow transactions with no meaningful economic link to the jurisdiction. The sovereignty in tax administration should not be used as an axe, but as a scalpel, removing only those elements that are not supported by the standard of global norms, by the constitutional notions of fairness, and by the image we are developing as a jurisdiction committed to rules. Let the law then serve not merely as a barrier to evasion, but as an enabler of lawful enterprise, penalising deception where it occurs, but encouraging legitimacy wherever it is found.

Cross-border corporate structuring shows how law responds to complex financial strategies. But legal boundaries appear in everyday speech too—read how humour can cross legal lines in “Can You Get Sued for a Joke?” on ElementLex.